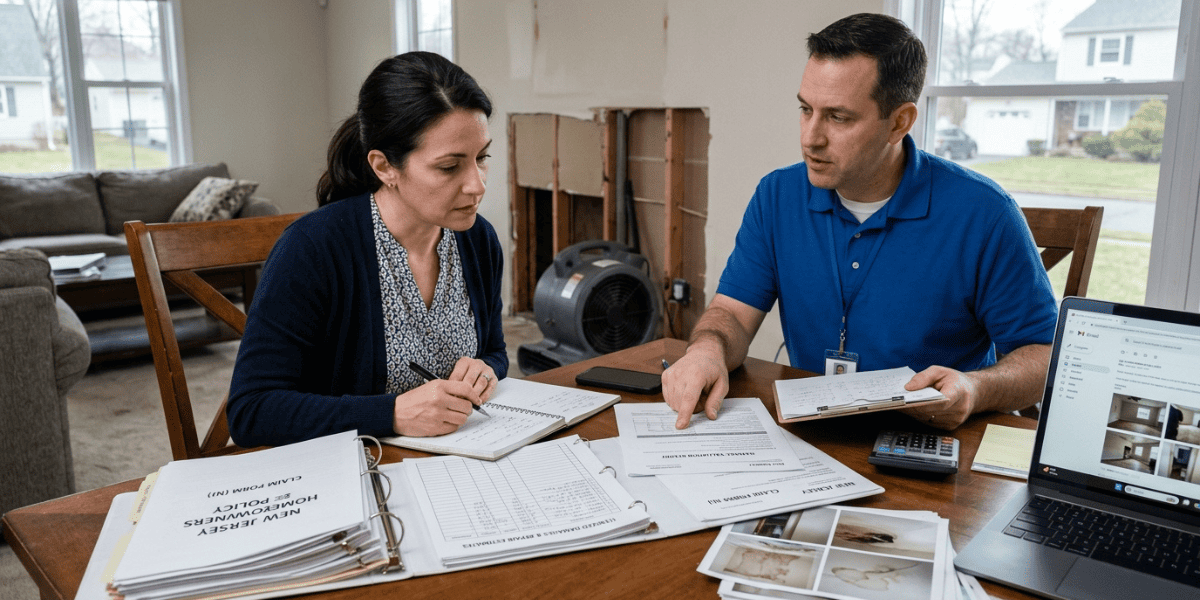

Filing a home insurance claim can feel stressful, especially after property damage disrupts daily life. Homeowners in New Jersey often face added pressure when insurance companies offer settlements that seem too low to cover actual repair costs. Storm damage, burst pipes, fire incidents, and theft claims can quickly become frustrating if the process is not handled carefully from the beginning.

A successful claim depends on preparation, organization, and understanding how insurers evaluate losses. Knowing what steps to take after damage occurs can help homeowners avoid delays, disputes, and underpaid settlements. Proper communication and strong evidence also make a major difference when negotiating with insurance companies.

This guide explains how you can protect your interests while filing a homeowners’ insurance claim in NJ and improve your chances of receiving a fair payout.

Understanding the Basics of a Home Insurance Claim

Home insurance policies are designed to help cover repair or replacement costs after certain types of damage. Policies typically include protection for the structure, personal belongings, liability, and additional living expenses if the home becomes temporarily unlivable.

However, insurance companies do not automatically pay the highest possible amount. Adjusters investigate damages, review policy limits, and calculate repair estimates before making settlement offers. Homeowners who fail to document losses properly may receive lower payouts than expected.

Reading the policy before filing a claim is important. Coverage limits, deductibles, exclusions, and reporting deadlines all affect the outcome of a claim. Understanding these details gives homeowners a clearer picture of what to expect during the process.

Steps to Take Immediately After Property Damage

The actions taken during the first 24 to 48 hours after damage can significantly affect claim results.

· Protect the Property from Further Damage

Insurance companies expect homeowners to prevent additional losses after an incident. Temporary repairs such as covering roof leaks, shutting off water, or boarding broken windows can help reduce further damage.

Keep all receipts for emergency repairs and supplies. These expenses may qualify for reimbursement under the policy.

· Document Everything Thoroughly

Photos and videos provide critical evidence during the claims process. Capture every affected area from multiple angles before cleanup or repairs begin.

Include:

- Structural damage

- Water intrusion

- Smoke or fire damage

- Damaged furniture and belongings

- Flooring and wall damage

- Appliance damage

Detailed records strengthen claim documentation and reduce disputes about the extent of losses.

· Create an Inventory of Damaged Items

List all damaged or destroyed belongings along with approximate purchase dates, brands, and estimated values. Receipts, bank statements, warranties, and previous photos of belongings can support ownership and value.

The more organized the information is, the more difficult it becomes for insurers to reduce payouts unfairly.

How do I File a Home Insurance Claim in NJ?

The claims process in New Jersey generally follows several important steps. Handling each step carefully can help homeowners avoid common mistakes that lead to reduced settlements.

· Contact the Insurance Company Quickly

Most insurance companies require prompt reporting after damage occurs. Delaying the claim could create complications or even result in denial.

Provide only factual information during the initial call. Avoid guessing about repair costs or the cause of damage if the situation is still unclear.

· Request a Claim Number and Adjuster Information

After reporting the loss, the insurer assigns a claim number and an insurance adjuster. Keep records of every phone call, email, and document shared throughout the process.

Written communication often helps prevent misunderstandings later.

· Review the Policy Carefully

Before discussing settlement figures, review the policy language carefully. Pay attention to:

- Coverage limits

- Deductibles

- Exclusions

- Replacement cost provisions

- Actual cash value clauses

· Get Independent Repair Estimates

One of the smartest ways to avoid underpayment is getting estimates from licensed contractors before accepting a settlement offer. Independent estimates provide a comparison against the insurer’s calculations. If contractor estimates are significantly higher, homeowners gain stronger negotiating power.

Common Reasons Insurance Claims Get Lowballed

Insurance companies often attempt to reduce claim payouts in several ways. Recognizing these tactics can help homeowners respond more effectively.

· Depreciation Calculations

Some policies pay actual cash value instead of replacement cost. This means insurers subtract depreciation based on the age and condition of damaged items. As a result, homeowners may receive far less than expected for older roofs, flooring, or appliances.

· Incomplete Damage Assessments

Adjusters sometimes overlook hidden issues such as water trapped behind walls, mold growth, or structural damage beneath flooring. Independent inspections can reveal problems that initial assessments miss.

· Low Contractor Pricing

Insurance companies may use pricing software that relies on average repair costs. Local contractors in New Jersey may charge more due to labor shortages, permit costs, or material pricing increases. Comparing estimates helps identify unrealistic pricing gaps.

· Policy Interpretation Disputes

Insurers occasionally argue that certain damages fall outside policy coverage. This commonly happens with flooding, wear and tear, or maintenance-related issues.

How do Insurance Adjusters Estimate Damage?

Insurance adjusters inspect property damage and calculate repair costs based on policy terms, inspection findings, and pricing databases. Their goal is to determine how much the insurance company should pay for the loss.

· Visual Inspections

Adjusters inspect affected areas, take photographs, and document visible damage. They may use moisture meters, drones, or specialized equipment depending on the situation. However, visible inspections do not always uncover hidden structural issues.

· Pricing Software

Many insurance companies use estimating software to calculate repair costs. These systems rely on regional averages for labor and materials. Problems can arise when software pricing does not reflect current market costs in New Jersey.

· Depreciation Formulas

Adjusters may reduce payouts based on the age and condition of damaged items. Roofs, siding, flooring, and appliances often receive depreciation deductions. Homeowners should request detailed breakdowns showing how depreciation was calculated.

· Contractor Comparisons

Insurance companies sometimes compare contractor bids against internal estimates. Large differences can trigger additional inspections or negotiations.

Providing detailed contractor proposals strengthens the homeowner’s position during settlement discussions.

What Documents Are Needed For a Home Insurance Claim?

Strong records improve claim accuracy and help homeowners challenge unfair settlement offers. Important documents include:

· Insurance Policy Documents

Keep copies of the full policy, declarations page, endorsements, and coverage summaries.

· Photos and Videos

Visual evidence taken immediately after the damage helps prove the severity of losses.

· Repair Estimates

Written estimates from licensed contractors support repair cost negotiations.

· Receipts and Invoices

Save receipts for temporary repairs, hotel stays, cleanup services, and replacement purchases.

· Inventory Lists

Detailed inventories of damaged belongings help support personal property claims.

· Communication Records

Store copies of emails, letters, and notes from phone conversations with adjusters and contractors.

How to Avoid Getting Lowballed on an Insurance Claim

Homeowners can take several steps to improve settlement outcomes and reduce the risk of unfair offers.

· Do Not Accept the First Offer Immediately

Initial settlement offers are not always final. Homeowners have the right to question calculations, request explanations, and submit additional evidence. Review every estimate carefully before signing anything.

· Hire Independent Professionals

Public adjusters, contractors, engineers, and restoration specialists can provide independent assessments of damage. Professional opinions often reveal missing repairs or underestimated costs.

· Keep Communication Professional

Emotional arguments rarely improve negotiations. Clear documentation and organized evidence create stronger leverage during claim discussions.

· Understand Replacement Cost Coverage

Replacement cost policies generally provide better reimbursement than actual cash value policies. Knowing the difference helps homeowners understand what compensation may be available.

· Request Reinspection if Necessary

Homeowners can ask for a further evaluation if more damage is found following the initial inspection. Supplemental claims are common after water damage, storm damage, and fire incidents.

· Know When Legal Help May Be Necessary

Some disputes require legal guidance, especially when insurers delay payments, deny valid claims, or refuse fair negotiations.

FAQs

· How long does a home insurance claim take in New Jersey?

The timeline depends on the complexity of the damage, inspections, and repair estimates. Simple claims may resolve within weeks, while large losses can take several months.

· Can a homeowner dispute a low insurance settlement offer?

Yes. Homeowners can submit additional repair estimates, request reinspection, or work with a public adjuster to challenge low offers.

· What should homeowners avoid saying to insurance adjusters?

Homeowners should avoid guessing about damage causes, minimizing losses, or making statements without complete information.

· Does filing a home insurance claim increase premiums?

Insurance claims can affect future premiums depending on claim history, damage type, and insurer policies.

· Should homeowners hire a public adjuster?

Public adjusters may help with large or complicated claims by providing independent evaluations and negotiating with insurance companies.

Conclusion

Filing a home insurance claim in New Jersey involves more than notifying the insurer about damage. Strong claim documentation, independent estimates, organized records, and a clear understanding of policy terms are key to fair compensation. Insurers evaluate every claim closely, and initial offers may not match real repair costs. Staying proactive, reviewing policy details, and providing solid evidence can significantly improve outcomes after property damage.

Contact Prime Insurance Services today to learn more about our reliable home insurance solutions that fit all types of property needs!